ELSS vs PPF: Which Tax-Saving Investment is Right for You?

Tax saving and wealth creation are two important financial goals for most investors. While there are several investment options available under Section 80C of the Income Tax Act, two of the most popular choices are Equity Linked Savings Scheme (ELSS) and Public Provident Fund (PPF).

Both offer tax benefits, but they differ significantly in terms of returns, risk, lock-in period, liquidity, and wealth creation potential.

Let’s compare ELSS and PPF to help you decide which option best suits your financial goals.

What is ELSS?

Equity Linked Savings Scheme (ELSS)ELSS is a category of mutual funds that primarily invests in a diversified portfolio of equity shares. It offers tax benefits under Section 80C while providing investors an opportunity to participate in the long-term growth of equity markets.

Over the years, ELSS has become one of the preferred investment options for investors seeking both tax savings and wealth creation.

What is PPF?

Public Provident Fund (PPF)PPF is a Government of India-backed long-term savings scheme designed to encourage disciplined investing and retirement planning.

It offers guaranteed returns, complete capital safety, and tax-free maturity benefits, making it a preferred investment option for conservative investors.

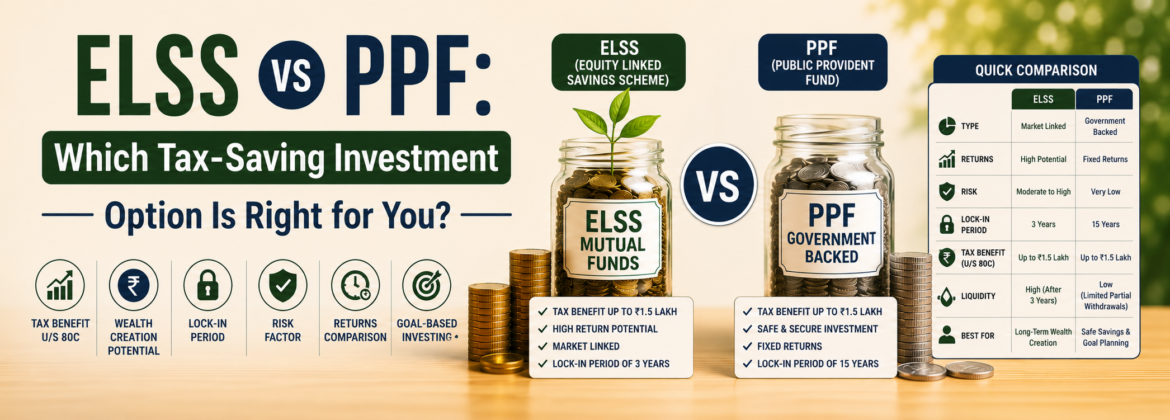

ELSS vs PPF: Key Differences

1. Investment Type

ELSS- Diversified Equity Mutual Fund.

- Invests primarily in equity shares.

- Market-linked returns.

- Government-backed savings scheme.

- Fixed-income investment.

- Designed for long-term savings and retirement planning.

2. Return Potential

ELSSReturns are market-linked and not guaranteed.

Historically, many ELSS funds have generated annualized returns in the range of 10% to 14% over long investment horizons, depending on market conditions and fund performance.

PPFReturns are declared by the Government of India and revised periodically.

Historically, PPF interest rates have generally ranged between 7% and 7.75%.

Winner for Growth Potential✅ ELSS, as equity investments have the potential to outperform fixed-income investments over the long term.

3. Risk Factor

ELSS- Market-linked investment.

- Returns are not guaranteed.

- Subject to equity market volatility.

- Backed by the Government of India.

- Guaranteed returns.

- Complete capital protection.

✅ PPF, making it suitable for conservative investors seeking stability.

4. Maximum Investment Limit

ELSSThere is no maximum investment limit. However, tax deduction under Section 80C is available only up to ₹1.5 lakh per financial year.

PPFMaximum investment allowed is ₹1.5 lakh per financial year.

Winner for Flexibility✅ ELSS, as investors can continue investing beyond the Section 80C limit for wealth creation.

5. Lock-In Period

ELSSLock-in period of only 3 years.

PPFLock-in period of 15 years.

Partial withdrawals are permitted after the prescribed period, subject to applicable rules.

Winner for Liquidity✅ ELSS, as it offers the shortest lock-in period among tax-saving investment options.

6. Tax Benefits

ELSS- Investment eligible for deduction under Section 80C up to ₹1.5 lakh.

- Long-Term Capital Gains (LTCG) up to ₹1.25 lakh per financial year are exempt.

- Gains above ₹1.25 lakh are taxed at 12.5%.

- Investment eligible for deduction under Section 80C.

- Interest earned is completely tax-free.

- Maturity proceeds are completely tax-free.

✅ PPF, as it enjoys the Exempt-Exempt-Exempt (EEE) tax status.

ELSS vs PPF: At a Glance

| Parameter | ELSS | PPF |

|---|---|---|

| Investment Type | Equity Mutual Fund | Government Savings Scheme |

| Returns | Market Linked | Fixed & Guaranteed |

| Expected Returns | 10%–14% (Historical) | 7%–7.75% |

| Risk | Moderate to High | Very Low |

| Lock-In Period | 3 Years | 15 Years |

| Maximum Investment | No Limit | ₹1.5 Lakh Per Year |

| Tax Benefit | Section 80C | Section 80C |

| Liquidity | Better | Limited |

| Wealth Creation Potential | High | Moderate |

Who Should Choose ELSS?

ELSS may be suitable if you:

- Want higher long-term return potential.

- Have a long-term investment horizon.

- Are comfortable with market fluctuations.

- Want tax savings along with wealth creation.

- Prefer investing through SIPs.

Who Should Choose PPF?

PPF may be suitable if you:

- Prefer guaranteed returns.

- Have a conservative risk profile.

- Want complete capital safety.

- Are planning for long-term goals such as retirement.

- Prefer predictable returns over market-linked growth.

Can You Invest in Both?

The Balanced ApproachMany investors do not necessarily have to choose between ELSS and PPF.

A balanced investment strategy may include:

- PPF for stability and capital protection.

- ELSS for long-term wealth creation and equity exposure.

This combination helps build a diversified portfolio that balances growth, safety, and tax efficiency.

Final Verdict

There is no universal winner between ELSS and PPF.

Your ideal choice depends on:

- Risk Appetite.

- Investment Horizon.

- Return Expectations.

- Financial Goals.

If your priority is capital protection and guaranteed returns, PPF may be the better choice.

If your objective is long-term wealth creation with potentially higher returns, ELSS can be more suitable.

For many investors, investing in both products provides the right balance between safety and growth.

Conclusion

Both ELSS and PPF are excellent tax-saving investments under Section 80C. While PPF offers stability, guaranteed returns, and complete tax-free maturity, ELSS provides the opportunity to build long-term wealth through equity market participation.

The key is to align your investment decisions with your financial goals, investment horizon, and risk tolerance.

Save Tax. Build Wealth. Invest Wisely.

Connect With Us

Suresh BhuraTruvestor Wealth

AMFI-Registered Mutual Fund Distributor

📧 Email: suresh@truvestor.net

📞 Phone: +91 9831119790

Disclaimer

Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. The information provided above is for educational purposes only and should not be construed as financial, tax, or investment advice. Tax laws and regulations may change over time. Investors should consult a qualified financial advisor before making investment decisions.

Leave A Comment